By Justine Irish D. Tabile, Senior Reporter

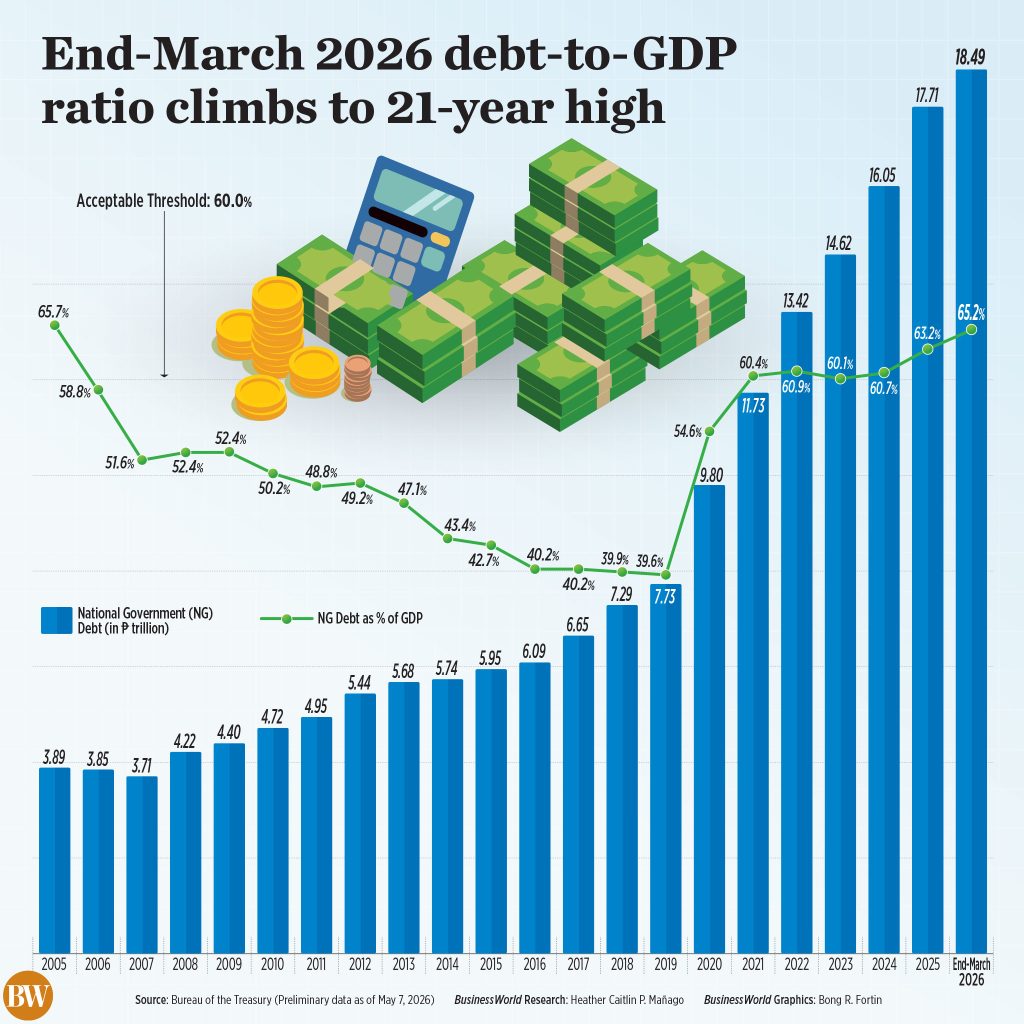

THE National Government (NG) debt as a share of gross domestic product (GDP) rose to 65.2% at the tip of the first quarter, the best ratio since 2005, data from the Bureau of the Treasury showed.

The rise got here as outstanding debt climbed by 1.8% to P18.49 trillion as of end-March from P18.16 trillion at the tip of February, while economic growth slowed sharply.

Philippine GDP expanded by 2.8% in the primary three months of 2026, the weakest pace because the pandemic, because the oil shock dampens consumer spending and stokes inflation.

Based on available data, the debt-to-GDP ratio at the tip of March was the best since 65.7% recorded in 2005. The debt-to-GDP ratio climbed to 63.2% at the tip of 2025.

This can also be above the 60% debt-to-GDP threshold considered by multilateral lenders to be manageable for developing economies.

“The recent uptick in NG debt partly reflects currency valuation effects somewhat than a pointy slippage in fiscal fundamentals as peso depreciation mechanically raises the peso value of foreign-currency obligations,” said Union Bank of the Philippines Chief Economist Ruben Carlo O. Asuncion in a Viber message.

“While peso weakness could proceed to place some upward pressure on headline debt figures amid global and geopolitical uncertainties, the impact should remain manageable given the federal government’s reliance on domestic, peso-denominated borrowing,” he added.

The peso closed P60.748 against the dollar on March 31, weakening by P3.083 from its P57.665 close on Feb. 27.

Domestic borrowings proceed to account for the majority of the debt stock, or 67.8%, while the remaining got here from external sources.

Domestic debt inched up by 0.44% to P12.53 trillion at end-March from P12.48 trillion at end-February, while external debt jumped by 4.81% to P5.95 trillion from P5.68 trillion.

“Even when most borrowing is domestic, peso depreciation will keep putting upward pressure on the debt stock so long as the West Asia situation and global financial uncertainty keep the dollar strong,” Jose Enrique “Sonny” A. Africa, executive director of the think tank IBON Foundation, said in a Viber message.

He added that the pressure on debt and costs would persist so long as the Philippines stays heavily depending on imports for fuel, food, and other consumer, intermediate and capital goods.

The local currency hit a record low of P61.567 on April 29.

To cushion the impact of the Middle East war on consumers, the federal government suspended excise taxes on liquefied petroleum gas and kerosene, while also rolling out subsidies and fuel discounts for vulnerable sectors.

Inflation accelerated to 7.2% in April, sharply faster than the 4.1% in March and 1.4% in the identical month last yr.

“The issue isn’t simply that NG debt is rising but how the federal government will create fiscal space needed to guard hundreds of thousands of poor and vulnerable Filipino households while also stabilizing the economy,” said Mr. Africa.

“The debt-to-GDP ratio will just worsen as growth slows and make the federal government’s fiscal conservatism ossify even further,” he added.

Mr. Africa said the federal government has to take a broader view of debt sustainability.

“This isn’t achieved by cutting support during a crisis but through the use of public finance to offer relief, support livelihoods, and stabilize the economy,” he added.

The NG’s outstanding debt is projected to achieve P19.06 trillion by end-2026 under the Budget of Expenditures and Sources of Financing 2026.

The federal government seeks to bring down the debt-to-GDP ratio to 58% by 2030.